WINTER WATCH

30-year government bond prices in the UK 🇬🇧 have fallen off of a cliff.

This is not “normal.” pic.twitter.com/rfVIZHWFHx

— The Kobeissi Letter (@KobeissiLetter) January 9, 2025

‘Great British Peso’ Plummets To 13-Month-Low As Investors Lose Faith In The UK https://t.co/J7uthbGJil

— zerohedge (@zerohedge) January 9, 2025

*****

RELATED

Where is Rachel Reeves?

WILL JONES

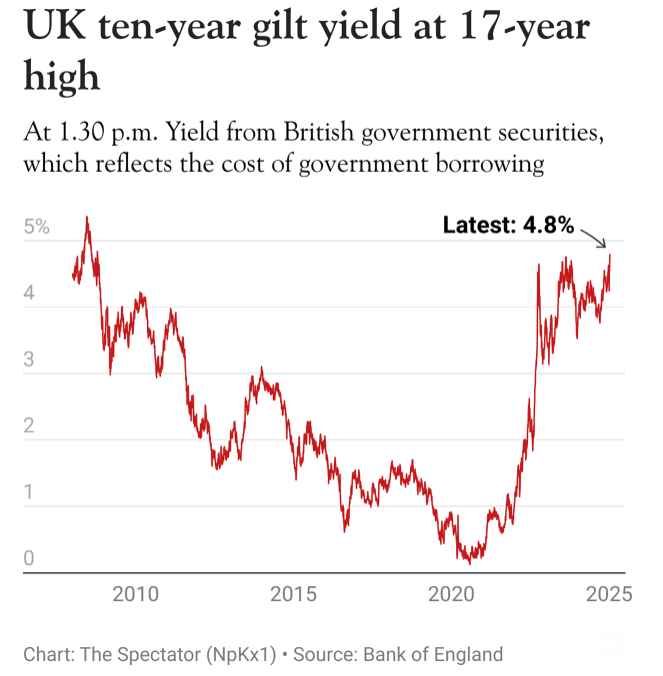

Bond yields are soaring to their highest levels in almost 30 years and sterling is sliding, but the Chancellor is nowhere to be seen. Where is Rachel Reeves and why won’t she address the markets her failed Budget has spooked, asks Matthew Lynn in the Spectator.

The Government’s economic strategy is facing its first real test, and where is the Chancellor? So far Rachel Reeves has been silent, preparing for a jaunt to China. At some point Reeves will have to address the markets – or risk turning a round of jitters into a full-blown crisis.

Over the last few days, the markets have turned decisively on the U.K. Yesterday, the yield on 10-year gilts hit its highest level since the financial crisis of 2008, while the yield on the 30-year gilt hit the highest level for 30 years. The U.K. is now paying more to service its debt than Greece, and very soon that will mean rising mortgage rates, and more companies going bankrupt. There is no mystery about what has happened. Investors have worked out that Reeves’s Budget, with its mix of big increases in borrowing, and higher company taxes, has failed, and will trap the economy in stagnation. The result? They are demanding more to lend money to the U.K.

Worth reading in full.

Meanwhile, Liz Truss has sent a cease and desist letter to Keir Starmer demanding that he stops claiming she crashed the economy, calling it “false and defamatory”. Her lawyers cite a report from economist Andrew Lilico, who tells the Telegraph that far from crashing the economy, “the thing that happened immediately following the mini-Budget was that the economy performed well”:

It’s not as though the economy was expected to go really fast and Liz Truss made it go a little bit slower than was expected. The thing that happened immediately following the mini-Budget was that the economy performed well. So it’s just preposterous to claim that she crashed the economy. Exactly the opposite happened. The economy did better than had been expected.

So Truss didn’t crash the economy, but Rachel from Accounts has.

*****

RELATED

Labour Britain is the new ‘PIGS’ of the global markets

The UK has carelessly exposed itself as the weakest link in the G7 at a perilous moment

AMBROSE EVANS-PRITCHARD

••••

The Liberty Beacon Project is now expanding at a near exponential rate, and for this we are grateful and excited! But we must also be practical. For 7 years we have not asked for any donations, and have built this project with our own funds as we grew. We are now experiencing ever increasing growing pains due to the large number of websites and projects we represent. So we have just installed donation buttons on our websites and ask that you consider this when you visit them. Nothing is too small. We thank you for all your support and your considerations … (TLB)

••••

Comment Policy: As a privately owned web site, we reserve the right to remove comments that contain spam, advertising, vulgarity, threats of violence, racism, or personal/abusive attacks on other users. This also applies to trolling, the use of more than one alias, or just intentional mischief. Enforcement of this policy is at the discretion of this websites administrators. Repeat offenders may be blocked or permanently banned without prior warning.

••••

Disclaimer: TLB websites contain copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available to our readers under the provisions of “fair use” in an effort to advance a better understanding of political, health, economic and social issues. The material on this site is distributed without profit to those who have expressed a prior interest in receiving it for research and educational purposes. If you wish to use copyrighted material for purposes other than “fair use” you must request permission from the copyright owner.

••••

Disclaimer: The information and opinions shared are for informational purposes only including, but not limited to, text, graphics, images and other material are not intended as medical advice or instruction. Nothing mentioned is intended to be a substitute for professional medical advice, diagnosis or treatment.

Disclaimer: The views and opinions expressed in this article are those of the author and do not necessarily reflect the official policy or position of The Liberty Beacon Project.

It is a near certain bet that Sir Keir Starmer will try to defy the bond vigilantes, hoping that global wealth funds will spot a bargain and start scooping up gilts at distressed prices without any need for Labour to change its current destructive course.

He may be lucky, but the international credibility of this Government is already shot below the water line. A few more days like this week’s rolling debacle will force his hand.

“Financial players think they were taken for a ride by Rachel Reeves in her pre-election charm offensives, and they don’t like it,” said Bernard Connolly, a veteran adviser to hedge funds and central banks, through multiple debt crises.

“Treasury reassurances will not help. The real fear in markets is that there is a vicious circle in which low growth worsens debt problems. They increasingly fear that the Government can’t get a grip. Something needs to happen to change the narrative,” he said.

Feeding Rachel Reeves to the sharks might placate some, but it “might also make them smell blood in the water”, he said. The larger fundamental problem remains.

“This Government seems hell bent on snatching defeat from every opportunity,” said Marc Ostwald, a bond specialist at ADM. “We were all hoping for stability after the incessant turmoil of the Tories, but it is now clear to markets that Labour don’t know what they are doing.”

The yield on 10-year gilts briefly touched 4.98pc on Thursday, nearing levels last seen in the late 1990s. “Once it slices through the psychological line of 5pc in a situation like this, the next stop can easily be 6pc. We’re not far away from the point when the Bank of England or the Treasury will have to come up with a circuit-breaker,” said Mr Ostwald.