")

BUDGET BRIEFING #2: Why has Britain’s relative economic decline been so precipitous?

THE UK’s relative and material economic decline can be pinpointed almost exactly to the onset of the Global Financial Crisis (GFC) starting in 2008. As demonstrated earlier that’s when the long term 2.3%pa per capita growth trend severely broke down. Proving exact cause and effect is of course complex with a number of factors at play, but since the GFC the UK has been stuck in a near death loop with negligible growth, as you will recall, the worst since records began 200 years ago.

Currently, the dominant narrative for this decline appears based on four primary arguments which can briefly be summarised as a) covid-19 impact b) the war in Ukraine c) public sector austerity and d) Brexit. Neat arguments, but as we shall show there are two big factors that are missing from this narrative, namely the impact of monetary policy and migration.

Further, of the dominant narrative four factors outlined above, in my view, only one has been truly material (covid-19) and another has some credence (war). Of those other narratives one is downright inaccurate (austerity) and the other is of virtually no consequence (Brexit). It is however essential to understand the reasons for the UK’s poor performance, for without understanding the cause a cure will be illusive.

It is the case that the UK, in common with much of the world, has been impacted by an unusual number of ‘black swan’ events over the last 15 years or so. The GFC stands as the watershed moment, in my view, changing the relationship between the state and those that it purported to govern. The post-GFC world has also been one of severe relative decline and stagnation.

In 2008 onwards, in an attempt to understandably avoid a 1930’s style depression, policy makers adopted a highly unusual monetary response of firstly reducing the cost of money with interest rates falling, in the UK case from around 5% to at the low 0.1%.

This was coupled with central banks adopting a novel approach of printing money (quantitative easing: QE) where authorities effectively bought their own Government debt with newly created funds. Between 2009 and 2016 the Bank of England created £445bn, or around 20% of GDP at that time. Internationally, other central banks did something similar.

The policy worked in as much as it stabilised the global economy but it had toxic side effects. It distorted asset prices, created arbitrary winners and losers (those who had assets generally enjoyed asset price inflation and those who didn’t were relatively left behind), encouraged inefficient asset allocation undermining sustainable growth and critically encouraged Governments to spend with less regard to balancing budgets funded by tax receipts. The age-old imperative to balance budgets prudentially had been broken.

The then Chancellor announced an ‘austerity programme’ signalling to markets the government was serious about ‘balancing the books.’ In reality however, while public spending was more effectively controlled than over the last five years public spending did not fall in real terms. Austerity was a myth put around to placate bond markets. Contrast that with, for example the Republic of Ireland where public sector salaries routinely fell by 20%. That is real austerity.

Coupled with this, the Bank of England, under Mark Carney, continued to run a policy of negative real interest rates, so a decade after the global financial crisis, they were still under 1% – a situation unprecedented in the 300-year history of the UK central bank.

Then comes the second black swan, covid-19 and the catastrophic response, lockdown, for the best part of two years. The response to enforced lockdown was to print a further £450bn through QE and crash interest rates to 0.1%. Effectively money was free.

The consequences of this were profound. Two years of highly negative growth with all the pain falling on the private sector, further economic distortions, societal change in terms of attitude to work (aided by furlough), significantly rising inactivity (over 9 million of working age now not working for a variety of reasons), a subsequent huge increase in migration and disruption to supply chains.

These factors started to fuel inflation, which had been largely absent before lockdown in goods (not assets or services) due to technology advances and let’s call it the China effect (cheap product from low cost economies.)

Coupled with the third black swan – war in Ukraine and the choice to sanction Russia which from an economic perspective – has fuelled domestic inflation while doing little to undermine the Russian economy, forced central banks to raise interest rates.

The impact of these three shocks and more importantly the response was to balloon the national debt, increase the size of the state at the expense of the productive private sector and create a belief amongst policy makers that they were God. They could effectively do as they pleased, spend as they liked and kick the can down the road pretending all was well.

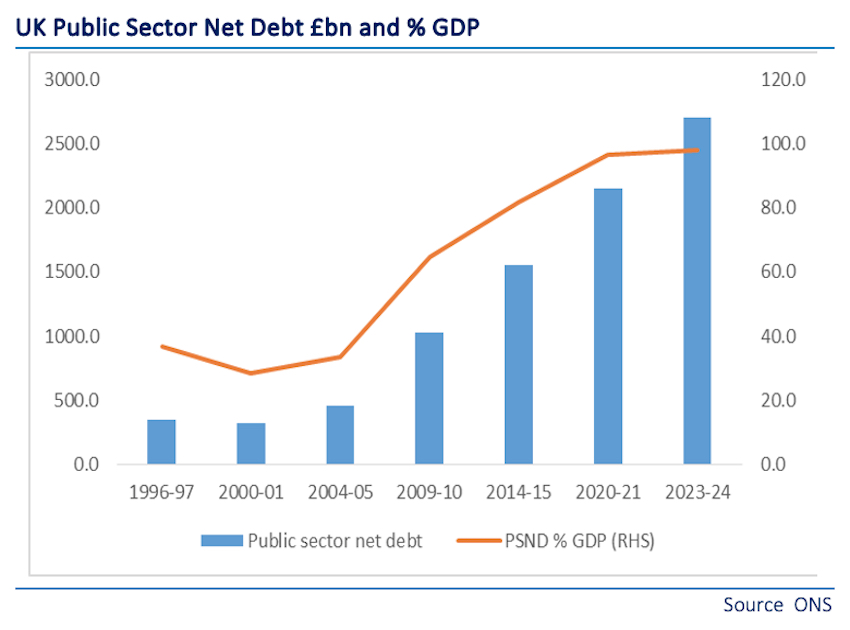

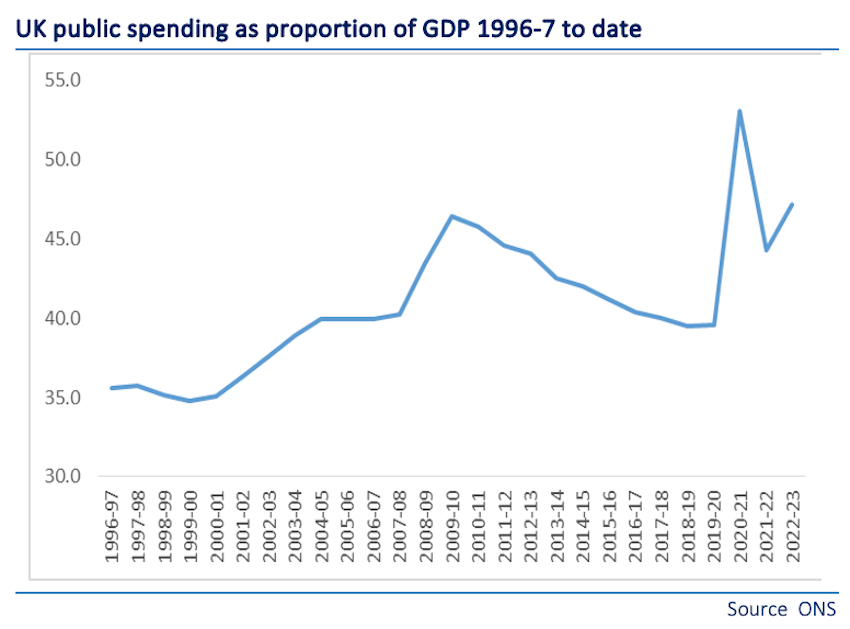

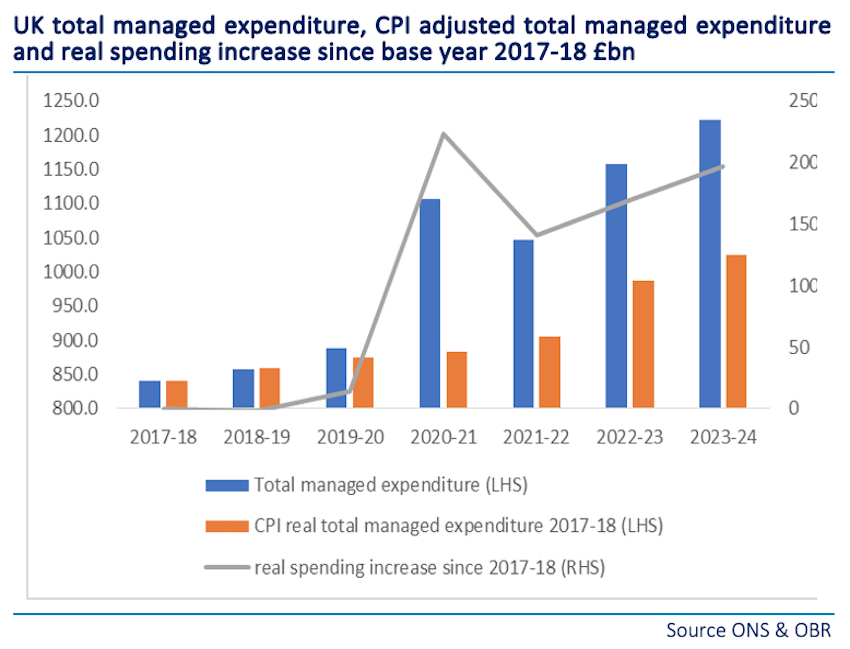

The four charts below highlight just how profound the change has been.

From a low level of public sector indebtedness before the GFC this has more than tripled in real terms in 20 years with the biggest peacetime increase in debt on record.

From a private sector that was almost two thirds of the economy in 2000 to almost half today.

And if there was no real austerity in the Osborne years there has been a glut since Johnson became PM with public spending increasing from £857bn in 2019 to £1222bn currently, a rise of almost £200bn in real terms since 2019 in exchange for public services noticeably failing.

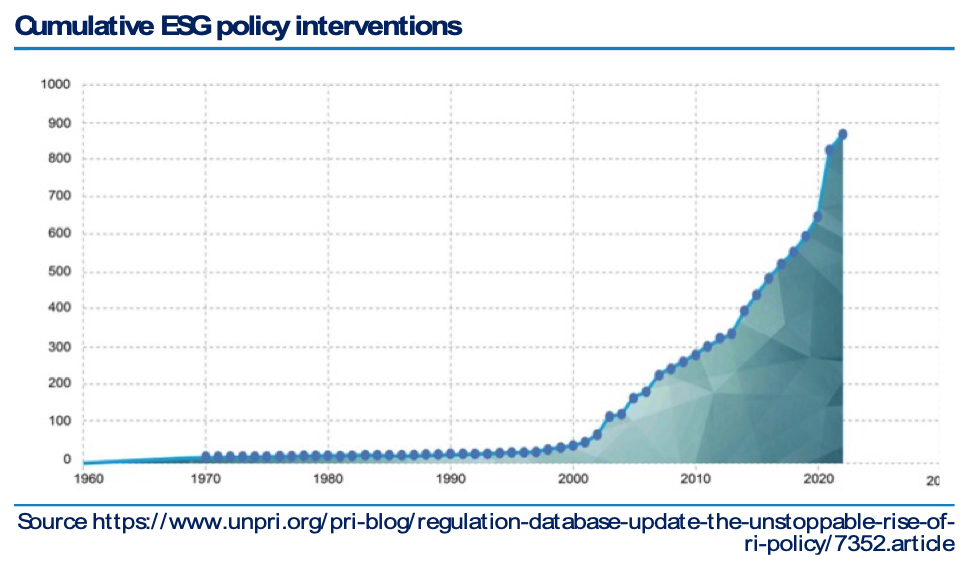

Effectively the UK has swapped a productive private sector for a low productivity unproductive public one and taken on board eye watering levels of debt. Worse, as we can see from the chart below what remains of the private sector is now regulated to an unprecedented extent. Hardly a sector is now not tightly regulated from energy to football, from banking to employment law and everything in between.

Some will argue that these were global phenomena thus it should have impacted all equally. The answer to that is the events might have had global impacts but the responses were generally national and the UK response was generally to spend, centralise and control to a far greater extent than most other countries. The UK chose its migration policy, it chose to regulate more than almost any other nation and it chose its response to lockdown in an absurdly expensive and inefficient manner.

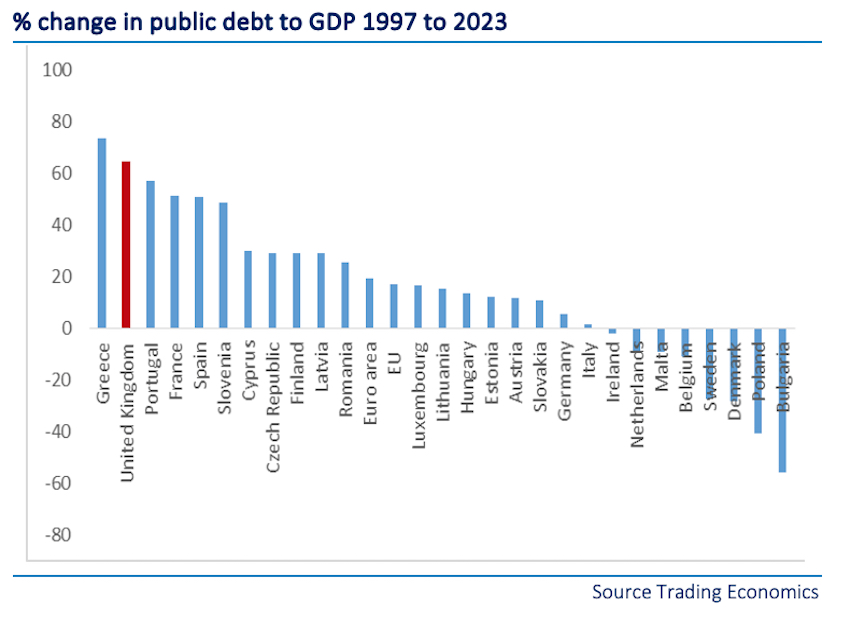

It is a matter of record that the UK has seen a greater deterioration in its public finances than any European nation bar Greece since 1997.

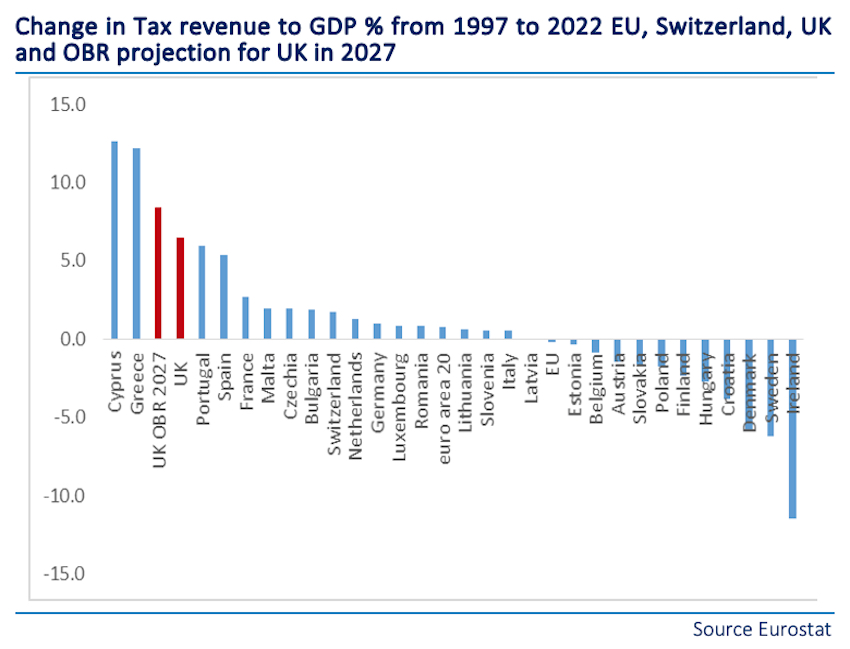

It is also a matter of record that bar Greece and Cyprus the UK has already raised the tax burden proportionately more than any European nation and that is before the likely increase that Rachel Reeves might have in mind. Many nations have actually cut tax over that period.

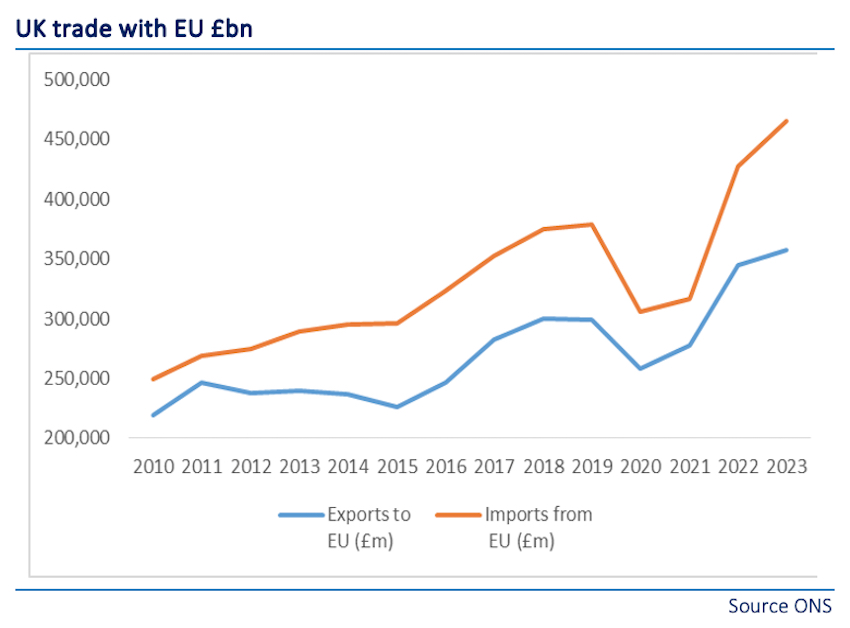

For those who think, well, it was Brexit, while the UK certainly has made poor choices and has not used the historic opportunity to create competitive advantage (quite the opposite) trade with the EU has increased by 45% since 2016. Frankly, regardless of ones views on the subject, Brexit’s impact is a rounding error compared with the GFC, lockdown, migration flows and the growth of the state and regulation.

Policy makers have radically changed the British economy over the last 20 years as a matter of choice. They have faced black swan events but the manner they have dealt with these challenges has been extreme by US and European standards.

There have been numerous poor choices but the most significant errors were failing to normalise monetary policy for over a decade after the GFC with inappropriately low interest rates and money printing and increasing regulation across the entire economy effectively controlling and centralising areas that would have seemed eccentric just a generation ago.

But the real straw that broke the camel’s back was the response to Covid-19 which embedded much higher public spending that ultimately has broken aspects of the nation’s work ethic, increased public debt markedly and resulted in much higher public spending with greatly inferior service. The result has been unprecedented levels of tax, squeezing the private sector further.

These factors have weighed heavily and squeezed growth out of the system. Austerity is a myth, sure the services are poor but that’s down to weak leadership, systemic failure and lockdown rationing service rather than money. Money has been thrown at the system to such an extent that public spending now equates to £42,000 per annum for each and every household in the land.

So, cantering through a brief history of the last 20-odd years we will next examine if the current Government is likely to improve the position or not.

This article ( BUDGET BRIEFING #2: Why has Britain’s Relative Economic Decline been so Precipitous?) was created and published by Global Britain and is republished here under “Fair Use” with attribution to the author Ewen Stewart

••••

Checkout TLBTalk.com:

Click Here to Visit the TLBTalk.com Site

••••

Welcome to the TLB Project Neighborhood

TLBTalk – Shake&Wake – The Liberty Beacon – The Butcher Shop

••••

The Liberty Beacon Project is now expanding at a near exponential rate, and for this we are grateful and excited! But we must also be practical. For 7 years we have not asked for any donations, and have built this project with our own funds as we grew. We are now experiencing ever increasing growing pains due to the large number of websites and projects we represent. So we have just installed donation buttons on our websites and ask that you consider this when you visit them. Nothing is too small. We thank you for all your support and your considerations … (TLB)

••••

Comment Policy: As a privately owned web site, we reserve the right to remove comments that contain spam, advertising, vulgarity, threats of violence, racism, or personal/abusive attacks on other users. This also applies to trolling, the use of more than one alias, or just intentional mischief. Enforcement of this policy is at the discretion of this websites administrators. Repeat offenders may be blocked or permanently banned without prior warning.

••••

Disclaimer: TLB websites contain copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available to our readers under the provisions of “fair use” in an effort to advance a better understanding of political, health, economic and social issues. The material on this site is distributed without profit to those who have expressed a prior interest in receiving it for research and educational purposes. If you wish to use copyrighted material for purposes other than “fair use” you must request permission from the copyright owner.

••••

Disclaimer: The information and opinions shared are for informational purposes only including, but not limited to, text, graphics, images and other material are not intended as medical advice or instruction. Nothing mentioned is intended to be a substitute for professional medical advice, diagnosis or treatment.

Leave a Reply